Institutional

Real Estate

East Africa

Mandate-based advisory for institutional investors seeking structured exposure to East African commercial assets.

Qualified Purchasers · Min. $5,000,000

$1.2B+

Assets Under Advisory

8.5–12.5%

Target Yield Range

2+

Years Active in Market

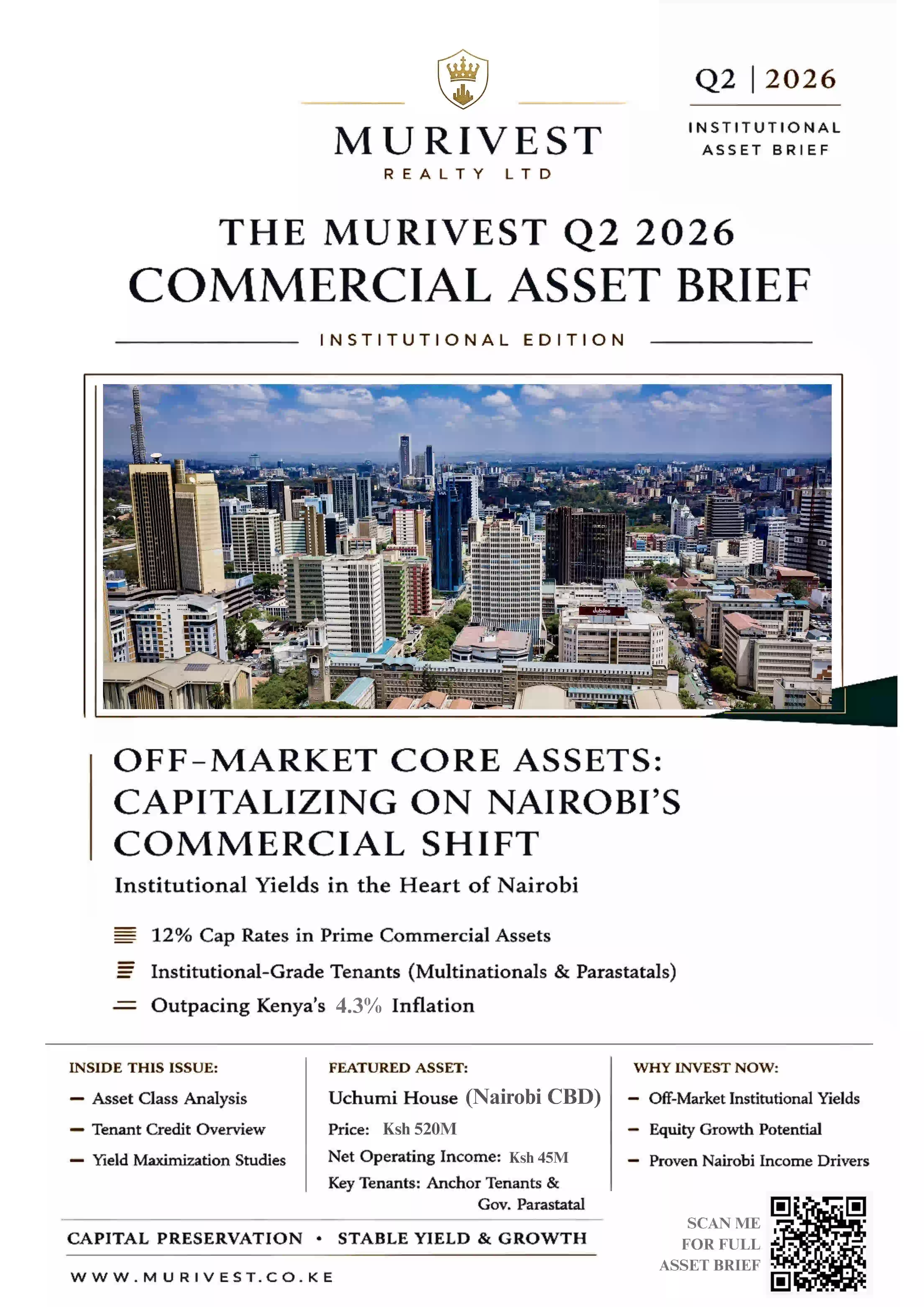

Nairobi Commercial Asset Brief

Institutional-grade overview of Nairobi commercial real estate opportunities, valuations, and capital positioning.

Verified investors only

Commercial Real Estate

Strategic Exposure

Murivest Realty Group advises across selected commercial real estate sectors aligned with urbanisation, infrastructure expansion, and institutional demand trends.

Income-Oriented Commercial Assets

Core Office Strategy

Institutional-grade office exposure supported by multinational tenancy demand and constrained Grade A supply dynamics.

Retail · Office Integration

Urban Mixed-Use Platforms

Diversified mixed-use positioning across high-density urban corridors with defensive occupancy characteristics.

Trade & Infrastructure Exposure

Logistics & Industrial Corridors

Industrial and logistics positioning aligned with East Africa’s evolving regional trade infrastructure.

Residential · Urban Living

Multi-Family Residential

Strategic positioning in multi-family residential assets to get consistent cashflows at the right location and refinance with increased rental rates and gain from capital appreciation.

Engagements conducted under formal advisory mandate and applicable regulatory compliance procedures.

Request Advisory EngagementInvestment System

Core Investment

Strategies

Murivest structures disciplined, mandate-based real estate strategies across three commercial asset classes — each selected for income durability, institutional governance, and risk-adjusted return profiles across East African cycles.

Core Office Market

Grade A Office Assets

Institutional-grade office buildings anchored by long-duration tenants across Nairobis prime commercial nodes — Westlands, Gigiri, and Karen. Focus on occupancy resilience and capital preservation through market cycles.

High-Yield Hospitality

Hospitality & Hotel Assets

Selective hospitality mandates in high-demand urban and tourism corridors. Underwriting prioritises RevPAR stability, operator covenant strength, and repositioning upside in supply-constrained markets.

Defensive Retail

Retail & Mixed-Use Hubs

Destination retail and integrated mixed-use centres anchored by essential-service tenants with strong catchment fundamentals. Positioned for income durability and structural demand from Kenya's expanding urban consumer base.

Core Office Market

Grade A Office Assets

Institutional-grade office buildings anchored by long-duration tenants across Nairobis prime commercial nodes — Westlands, Gigiri, and Karen. Focus on occupancy resilience and capital preservation through market cycles.

High-Yield Hospitality

Hospitality & Hotel Assets

Selective hospitality mandates in high-demand urban and tourism corridors. Underwriting prioritises RevPAR stability, operator covenant strength, and repositioning upside in supply-constrained markets.

Defensive Retail

Retail & Mixed-Use Hubs

Destination retail and integrated mixed-use centres anchored by essential-service tenants with strong catchment fundamentals. Positioned for income durability and structural demand from Kenya's expanding urban consumer base.

"The best investment on Earth is earth — structured, mandated, and protected."

View Full PortfolioInstitutional Standards

Exit Strategy &

Risk Engineering

In Kenyan commercial real estate, losses rarely come from market cycles — they come from structural failures: title defects, poor exit planning, and regulatory exposure. Murivest structures the exit before acquisition, ensuring every asset is engineered for controlled liquidity and capital protection.

7 – 10

Year Hold Horizon

Exit Is Designed at Entry

Institutional capital globally now holds assets for 6–7 years on average. Murivest pre-defines exit timing, buyer profile, and disposal pathway at mandate inception so every lease and capital decision aligns with exit value creation.

McKinsey Global Private Markets Report 2026

40%

of Land Fraud Cases in Kenya

Title Risk Is Structural

Land-related fraud remains the dominant form of financial loss in Kenya’s property market, with over 10,000 active investigations. Every mandate begins with forensic title verification, encumbrance checks, and regulatory compliance screening.

EACC 2023 · Ministry of Lands Kenya 2024

3

Exit Structures

Liquidity Is Engineered

Exit is structured through institutional sale, recapitalisation, or sale-leaseback mechanisms depending on asset profile. Each route is designed for tax efficiency, compliance alignment, and capital mobility under IFRS standards.

McKinsey GPM 2025 · IFRS 16 · KRA CGT Framework

“Capital without structured exit design is exposure, not investment.”

Request Exit BriefMarket Intelligence · Q2 2026

Nairobi Commercial

Real Estate Intelligence

Nairobi's commercial market is undergoing structural rebalancing. Capital is concentrating in Grade A office, logistics, and mixed-use corridors, while secondary stock continues to dilute pricing power and occupancy across the metro area.

Grade A Office

Westlands · Gigiri · Karen

Compressing

Westlands leads absorption — flight-to-quality demand accelerating

Industrial & Logistics

Nairobi · Tatu City · JKIA Zone

Tightening

Structural demand expansion from e-commerce and agro-logistics

Retail — Destination Centres

Kilimani · Westlands · Karen

Stable

Selective node strength — anchor-tenant covenants remain resilient

Mixed-Use Development

Integrated Assets

Outperforming

Highest blended yield — diversified income structure

Grade A Office

Westlands · Gigiri · Karen

Yield

8.5%

Vacancy

19.3%

Signal

Compressing

Westlands leads absorption — flight-to-quality demand accelerating

Industrial & Logistics

Nairobi · Tatu City · JKIA Zone

Yield

9.5%

Vacancy

17.0%

Signal

Tightening

Structural demand expansion from e-commerce and agro-logistics

Retail — Destination Centres

Kilimani · Westlands · Karen

Yield

8.4%

Vacancy

19.8%

Signal

Stable

Selective node strength — anchor-tenant covenants remain resilient

Mixed-Use Development

Integrated Assets

Yield

8.4%

Vacancy

~18.5%

Signal

Outperforming

Highest blended yield — diversified income structure

Grade A assets continue to outperform across Westlands, Gigiri, and Karen, driven by tenant consolidation and flight-to-quality dynamics. Industrial logistics remains the strongest structural allocation theme in Kenya, supported by sustained regional distribution and e-commerce demand.

Mandated intelligence only · KYC required · Q2 2026

Request Full Intelligence PackInvestment Framework

Five Principles

One Objective

Capital in this market is rotating faster than at any point in the last decade. The question is not whether it moves — but whether it moves into structure or exposure.

Income That Endures. Not Appreciation That Disappears.

Capital is rotating away from lifestyle property into income-producing commercial assets. Knight Frank confirms a structural reallocation: primary residence exposure collapsed in a single year. The implication is simple — capital that does not enter structured income assets is left exposed to informal mid-market risk and construction-sector stress.

Knight Frank Wealth Report 2025

Market Philosophy

22%

HNWI wealth in primary homes

↓ from 50–60% (2024)

Income That Endures. Not Appreciation That Disappears.

Capital is rotating away from lifestyle property into income-producing commercial assets. Knight Frank confirms a structural reallocation: primary residence exposure collapsed in a single year. The implication is simple — capital that does not enter structured income assets is left exposed to informal mid-market risk and construction-sector stress.

Knight Frank Wealth Report 2025

Where the Data Points Before the Market Arrives.

Industrial real estate is the strongest structural signal in the market. Occupancy across Africa reached a decade high, driven by e-commerce and agro-logistics demand. In Nairobi, Grade A logistics assets continue to show yield premium and supply constraints relative to demand.

Knight Frank Africa Industrial H1 2025

Asset Selection

9.5%

Prime logistics yield — Nairobi

83% Africa warehouse occupancy

Where the Data Points Before the Market Arrives.

Industrial real estate is the strongest structural signal in the market. Occupancy across Africa reached a decade high, driven by e-commerce and agro-logistics demand. In Nairobi, Grade A logistics assets continue to show yield premium and supply constraints relative to demand.

Knight Frank Africa Industrial H1 2025

Downside Protection Is the Strategy.

Every acquisition is stress-tested beyond current market conditions, including vacancy expansion and rent compression scenarios. Capital preservation is not assumed — it is engineered. This discipline reflects broader private market reality where operational resilience now drives returns more than leverage.

Murivest Underwriting Framework

Risk Discipline

5–8pp

Vacancy stress test buffer

Murivest underwriting standard

Downside Protection Is the Strategy.

Every acquisition is stress-tested beyond current market conditions, including vacancy expansion and rent compression scenarios. Capital preservation is not assumed — it is engineered. This discipline reflects broader private market reality where operational resilience now drives returns more than leverage.

Murivest Underwriting Framework

Leverage Amplifies Returns — and Risk.

Global commercial real estate stress highlights the cost of aggressive leverage cycles. Underwater loan exposure in major markets reinforces a structural shift: debt must be sized to income resilience under stress, not optimistic pricing cycles.

MSCI Real Estate in Focus 2025

Capital Structure

14%

US CRE loans underwater (2025)

~$500B exposed globally

Leverage Amplifies Returns — and Risk.

Global commercial real estate stress highlights the cost of aggressive leverage cycles. Underwater loan exposure in major markets reinforces a structural shift: debt must be sized to income resilience under stress, not optimistic pricing cycles.

MSCI Real Estate in Focus 2025

UHNW Capital Requires Infrastructure.

UHNW capital behaves differently — it requires access, structuring, and governance. Institutional managers increasingly compete on access to private capital networks, not just deal flow. Murivest operates within that framework: off-market access, structured entry, defined exit.

Knight Frank / McKinsey Wealth Data

Investor Access

0.003%

Global population (UHNWIs)

Control > 1/3 global private wealth

UHNW Capital Requires Infrastructure.

UHNW capital behaves differently — it requires access, structuring, and governance. Institutional managers increasingly compete on access to private capital networks, not just deal flow. Murivest operates within that framework: off-market access, structured entry, defined exit.

Knight Frank / McKinsey Wealth Data

This framework is applied only to mandated capital relationships. Every allocation is reviewed against downside protection, exit clarity, and structural resilience before execution.

Request AccessEnvironmental · Social · Governance

ESG Framework

Capital Risk Lens

ESG at Murivest is not a reporting function — it is a capital protection filter. It determines what is investable, what is bankable, and what is institutionally acceptable before capital is deployed into East African real estate markets.

100%

ESG-Screened Mandates

3+

Framework Benchmarks

GRI / IFRS

Reporting Standards

Environmental

Responsible Investment Integration

Environmental, social, and governance considerations are embedded directly into underwriting rather than treated as post-investment reporting. Each mandate is screened through a risk-adjusted lens consistent with institutional capital expectations, including PRI-aligned frameworks where applicable.

Social

Built Asset Sustainability Standards

Asset selection prioritises measurable efficiency in energy use, water consumption, and embodied carbon. Where applicable, developments are assessed against IFC EDGE and LEED frameworks, with emphasis on climate resilience and long-term operating cost stability.

Governance

Institutional Governance & Reporting

Each mandate is structured with formal governance controls, legal compliance verification, and reporting frameworks aligned with institutional investor requirements. ESG and financial performance are tracked in parallel where required for fiduciary reporting obligations.

Long-duration capital requires long-duration stewardship. ESG is not an overlay — it is structure.

View Full ESG FrameworkExecutive Leadership

Mark Muriithi

Chief Executive Officer · Founder

“Institutional capital is not deployed for momentum — it is allocated for durability. Downside protection precedes structure. Structure precedes return.”

Mark Muriithi founded Murivest Realty Group in 2025 to bridge institutional capital and Kenya’s commercial real estate market through structured advisory, disciplined underwriting, and off-market execution.

His background spans commercial real estate, distribution, and technology — experience that informs Murivest’s approach to deal origination, asset positioning, and investor execution. Earlier roles at Vineyard Properties provided direct exposure to transactional real estate markets, while subsequent commercial leadership roles strengthened capital markets literacy and network depth across East Africa.

Murivest is structured to align with institutional expectations: underwriting discipline, governance transparency, ESG awareness, and reporting standards consistent with pension funds and family offices.

Independent Advisory Platform

Mandate-based engagements · Institutional underwriting standards · Fiduciary alignment

API Global

United Kingdom · Est. 2004

Baron & Cabot

United Kingdom · Est. 2014

Knight Frank

Kenya · Est. 1896

Pam Golding

Kenya · Est. 1976

Black Standard — Private lifestyle infrastructure partner providing UHNW mobility coordination, aviation access, concierge services, security orchestration, and global residence logistics through a discreet, invitation-based network.

Non-public access layer · Discretion-first execution · Invitation-only coordination

Visit Strategic PartnerRegulatory Framework & Disclosures

Mandate Documentation Required

All engagements governed by formal mandate agreements defining scope, liability, and execution terms prior to advisory commencement.

KYC / AML Compliance

Full identity and source-of-funds verification required for all capital partners prior to any advisory or transaction engagement.

No Collective Investment Schemes

Murivest does not pool capital or operate regulated investment funds. Strictly advisory services on a mandate basis only.

Murivest Realty Group Ltd is an independent commercial real estate advisory platform. All engagements are subject to formal mandate agreements, independent due diligence, and regulatory compliance frameworks applicable in Kenya and international jurisdictions.